A Guide to Modern Insurance Risk Management

A Guide to Modern Insurance Risk Management

Explore modern insurance risk management. This guide covers how top AI insurance companies use AI for claims automation, customer care, and ERM.

For a long time, insurance risk management was seen as a purely defensive game—a necessary cost center focused on preventing losses. That view is officially outdated. Today, for any insurer looking to grow, it's about turning risk into a strategic advantage, helping navigate economic turbulence and meet sky-high customer expectations.

The New Era of Insurance Risk Management

The modern insurance world is a pressure cooker. We're facing everything from escalating catastrophe losses to a hyper-competitive market that leaves zero room for error. In this environment, the most forward-thinking AI insurance companies aren't just using technology for a bit of efficiency. They're weaving it into the very fabric of their risk strategy.

Think of it like a captain navigating a complex shipping route. A basic radar helps you avoid icebergs (the old way of seeing risk). But an advanced, AI-powered navigation system? That not only steers you clear of danger but also charts the fastest, most fuel-efficient path to your destination, revealing opportunities you never knew existed.

This proactive mindset is no longer optional; it's essential for survival. The industry is staring down a massive and growing "protection gap," where the economic fallout from disasters wildly outstrips what's actually insured. This puts immense strain on the old ways of doing business.

Navigating Unprecedented Volatility

The numbers really tell the story here. In a recent year, natural catastrophes caused an estimated $357 billion in economic losses. The shocking part? Only about 35% of that was insured.

That left a staggering $234 billion protection gap, a clear signal that the industry's existing capacity and models are being stretched to their limits. And the volatility is only getting worse. In the first half of the following year, insured losses from natural disasters shot past $100 billion, a jarring 40% jump from the year before. This isn't a minor fluctuation; it's a trend that demands a complete rethink of how we handle risk, capital, and pricing.

Regulators are taking notice. They're now flagging climate-related exposures, persistent cyber threats, and geopolitical instability as top-tier concerns, pushing insurers to get much more sophisticated with their scenario analysis and cross-border planning.

AI as the New Bedrock of Operations

So, how do you manage these pressures without buckling? The answer lies in smarter operations, powered by automation. AI is quickly becoming the go-to solution for overhauling two of the most critical functions in financial services: claims processing and customer care.

By automating the intricate, often frustrating workflows in these areas, insurers can slash cycle times, boost accuracy, and build the kind of customer loyalty that was once impossible to achieve at scale. This isn't just about managing day-to-day tasks; it's a fundamental part of building a more resilient and profitable business. You can learn more about how risk management is applied in operations in our detailed guide.

Platforms that deliver on AI customer care and claims automation are no longer a "nice-to-have." They are the foundation for the future of insurance.

Building a Resilient ERM Framework

Think of a modern Enterprise Risk Management (ERM) framework as the essential blueprint for any successful insurer. It’s what transforms risk management from a scattered, reactive scramble into a unified, firm-wide strategy. This framework is the structure that gives you the discipline and foresight needed to navigate the complexities of underwriting, pricing, and claims.

At the heart of any strong ERM is a clearly defined risk appetite. This isn't just a number; it’s a guiding philosophy. It clearly states the amount and type of risk your organization is willing to take on to hit its strategic goals. Without it, an insurer is essentially flying blind, unable to tell the difference between a calculated risk and a reckless gamble.

Navigating Market Cycles and Pricing Pressures

This disciplined approach is absolutely critical when market conditions shift—and they always do. Take the commercial insurance pricing cycle, for instance. It can force dramatic changes in underwriting tactics. We saw this recently when the market softened considerably, with one report noting a 4% drop in global commercial insurance rates in a single quarter, ending a seven-year streak of increases.

That kind of shift signals intense competition and a flood of capacity, which puts direct pressure on premiums and underwriting margins. In response, many insurers are pulling back on their risk-taking. A recent survey found that only 12% of insurers were looking to increase risk, while 67% were actively exploring alternative capital structures like reinsurance sidecars to better manage their exposures. These are the kinds of measurable market movements that force carriers to get much sharper with their risk selection and expand their capital management toolkit just to stay profitable.

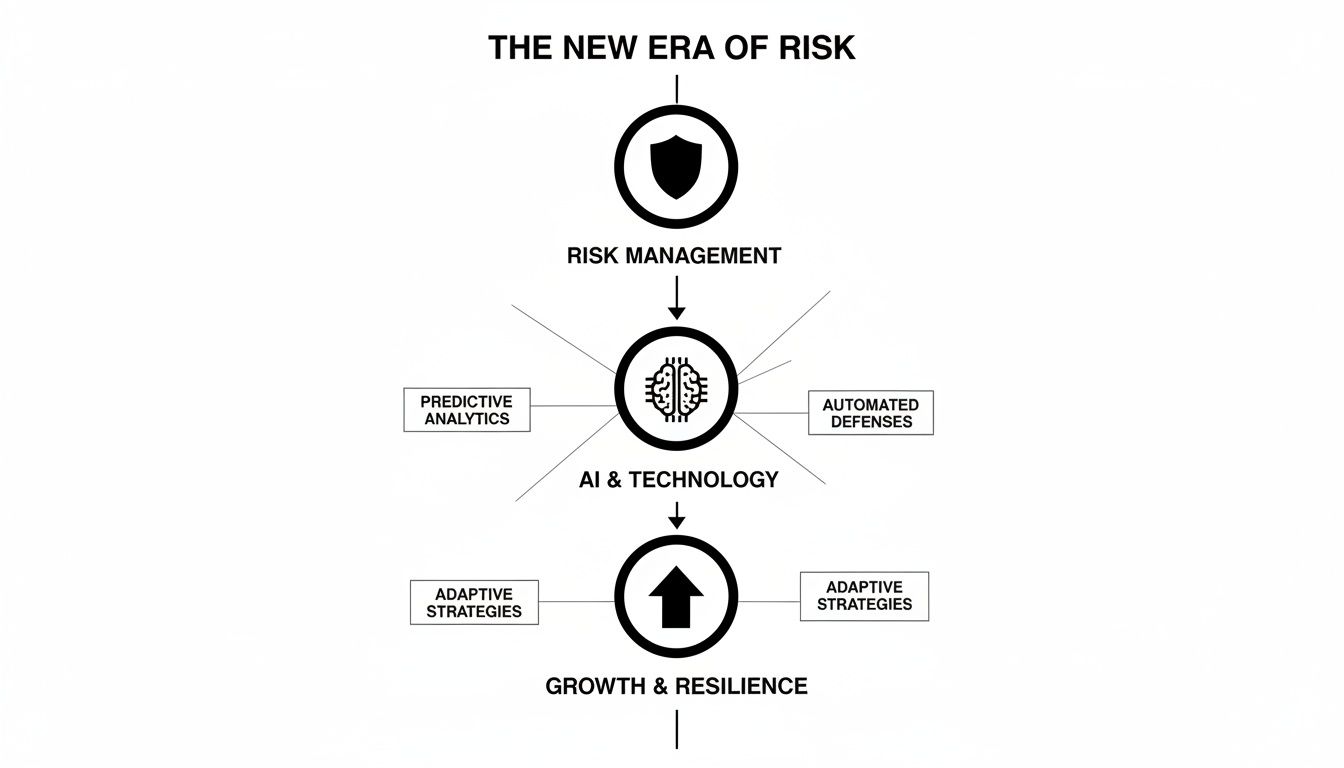

The chart below shows how a modern risk framework can integrate technology, like AI, to build resilience and drive growth, even in a tough market.

This visual really clarifies the hierarchy: foundational risk management principles are amplified by AI and technology, which together enable a company to grow and become more resilient.

The Three Lines of Defense Model

To actually put a framework like this into practice, leading insurers rely on the "three lines of defense" model. It’s a governance structure that clarifies exactly who is responsible for what when it comes to managing risk across the entire organization.

First Line: This is your front line—the business operations teams like underwriters and claims handlers. They own and manage their risks directly and are responsible for identifying and controlling them day-to-day.

Second Line: The risk management and compliance functions act as the second line. They provide oversight, setting the policies and frameworks that guide the first line's activities.

Third Line: Internal audit serves as the independent third line. They provide objective assurance that the first two lines are working effectively and that the overall framework is sound.

This model is all about accountability. It creates a system of checks and balances that prevents critical risks from falling through the cracks, which is vital for maintaining stability, especially as more core processes become automated.

By using a well-defined framework to assess potential threats, you can establish clear priorities for mitigation. For a practical look at how this works, you can see a risk assessment form template AI-generated example to better understand the process.

How AI Is Transforming Claims And Customer Care

For decades, the insurance claims process has been a major friction point. It's often slow, manual, and frankly, a frustrating experience for everyone involved—policyholders and insurers alike. Artificial intelligence is now completely flipping that script. We're moving away from reactive, paper-heavy workflows and toward automated, proactive systems that are a game-changer for insurance risk management.

This isn't just about shaving off a few operational costs. By automating core tasks, AI is fundamentally redefining what's possible in speed, accuracy, and customer satisfaction. The entire journey of a claim, from the first call to the final payment, is being rebuilt from the ground up for a smarter, more efficient world.

This is the new front line of claims. A customer can now snap a photo, and that simple action can trigger a fully automated assessment, feeding data straight into an intelligent workflow.

Automating The Claims Lifecycle With AI

The claims experience is the moment of truth for any insurer. A clunky, drawn-out process can shatter a customer relationship in an instant. But a fast, transparent, and simple one can build loyalty that lasts a lifetime. AI agents are now being deployed at every single stage of this critical journey.

Here’s where the automation is making the biggest impact:

First Notice of Loss (FNOL): AI chatbots and voice assistants work around the clock, handling the initial claim intake 24/7. They gather all the essential details and documents, so a human adjuster doesn't have to.

Damage Assessment: Forget waiting for an adjuster to schedule a visit. Computer vision AI can analyze photos and videos of damage to a car or home, generating a repair estimate almost instantly.

Fraud Detection: AI algorithms are incredibly good at spotting red flags. They can sift through thousands of data points in real-time to identify suspicious patterns that a person would almost certainly miss.

Settlement and Payment: For straightforward claims, AI can run the show from start to finish, automating settlement and getting money into a policyholder's hands in a matter of hours, not weeks.

This rapid shift toward AI is also forcing a rethink of operational risk. One recent survey found that 55% of insurers now list risk management and analytics as a top investment priority. Insurers are pouring money into better data and automation to shrink loss ratios, but they're also wisely investing in the governance and control systems needed to ensure AI doesn't introduce brand-new risks.

Delivering Superior AI Customer Care

The impact of AI extends well beyond just claims. It’s also completely changing the game for customer service in financial services. Today’s policyholders expect immediate, helpful answers, and AI is delivering.

Instead of sitting on hold, customers can now interact with intelligent AI agents that provide instant, personalized support. These agents can tap into an insurer’s entire knowledge base to answer complex policy questions, process account changes, or even offer advice on coverage—all with a consistent and helpful tone.

A smart "human-in-the-loop" design is key here. The AI handles the high volume of routine questions, but it’s trained to know exactly when to escalate a conversation to a human expert for situations that require real empathy or complex judgment.

This frees up human agents to focus on the high-stakes, emotionally charged interactions where their expertise truly matters. The payoff is a much better customer experience, which shows up in higher Net Promoter Scores (NPS). To see how this works in practice, you can get more details in our guide on AI in insurance claims.

The table below shows a clear before-and-after picture of how AI-powered platforms like Nolana are overhauling traditional insurance operations.

AI Impact on Insurance Operations

Operational Area | Traditional Process (Manual) | AI-Automated Process (e.g., with Nolana) | Key Performance Indicator (KPI) Impact |

|---|---|---|---|

Claims Intake (FNOL) | Phone calls, manual data entry, business hours only. | 24/7 intake via chatbot/voice, automated data extraction. | -30% call center volume, +50% intake speed. |

Damage Assessment | Manual review by adjusters, scheduling physical inspections. | Instant analysis of photos/videos with computer vision AI. | -90% assessment time (days to minutes). |

Fraud Detection | Manual review, reliance on adjuster suspicion. | Real-time analysis of claim data to flag anomalies. | +25% fraud detection rate, reduced false positives. |

Customer Service | Long hold times, agent-dependent knowledge, limited hours. | Instant 24/7 support, AI-powered knowledge base access. | -40% in operational costs, +20% NPS. |

As you can see, the improvements aren't just incremental; they represent a fundamental shift in efficiency, accuracy, and customer satisfaction across the board.

The Power Of Integration And Fraud Prevention

Of course, for any of this to work, AI systems have to play nice with an insurer's existing core platforms, like Guidewire or Duck Creek. This is where modern agentic platforms like Nolana shine. They are designed to act as an intelligent layer that sits on top of legacy technology. This means they can pull information, help with decisions, and execute tasks without forcing a hugely expensive and disruptive "rip-and-replace" project.

This integration also bolsters one of AI’s most powerful applications: fraud prevention. By connecting disparate systems, AI can verify identities and authenticate documents with incredible precision. For example, new tools are using a Bluenotary's biometric-first approach to reducing fraud risk to add a serious layer of security to digital claims. By automating these crucial checks, insurers can manage risk far more effectively, protecting their bottom line and their honest customers.

Implementing AI Safely in a Regulated Industry

Bringing artificial intelligence into a field as heavily regulated as insurance is about much more than just plugging in new software. You’re navigating a careful balance between earning trust, proving the tech is reliable, and making sure every single automated action meets strict compliance standards. For AI insurance companies, the only path forward is one built on strong governance and a clear, responsible strategy.

What this really means is building a framework where AI doesn’t just operate inside a black box. Every decision must be traceable, explainable, and fully auditable. This is where concepts like Explainable AI (XAI) become so critical, giving risk and compliance teams the ability to see the "why" behind any AI-driven recommendation.

Building a Human-in-the-Loop System

There's a common myth that AI automation is all about replacing people. In a high-stakes industry like insurance, nothing could be further from the truth. The most effective—and safest—approach is a "human-in-the-loop" system, where AI and human experts work together, each playing to their own unique strengths.

Think of it as a finely tuned partnership. AI agents can chew through high-volume, data-heavy tasks with incredible speed and accuracy, like reviewing initial claim documents, flagging potential fraud indicators, or handling routine policy questions. But they operate with very clear guardrails.

The moment a case involves unusual complexity, high financial stakes, or requires a dose of genuine human empathy, the AI is programmed to seamlessly escalate it to a person. This ensures that while routine work gets automated, critical judgment always stays in human hands—a cornerstone of responsible insurance risk management.

This blended approach isn’t just a safety net; it’s a powerful strategic advantage. It frees up your skilled adjusters and service agents to focus their expertise on the most complex and valuable work, which ultimately improves both efficiency and customer outcomes.

The Critical Role of Governance and Compliance

For any insurer, deploying AI without an ironclad compliance foundation is simply not an option. Regulators demand transparency, and customers (rightfully) expect their data to be handled with the utmost security. This is precisely why platforms designed for regulated industries are built with compliance baked in from the very start.

Agentic platforms like Nolana, for example, are architected to meet rigorous standards from day one. This means achieving certifications that are table stakes for earning enterprise trust.

SOC 2 Compliance: This is proof of a commitment to securely managing customer data to protect both your organization and your clients' privacy. You can get a better sense of its importance by learning about what SOC 2 compliance is and why it’s a benchmark for any serious service provider.

GDPR Compliance: For any insurer touching the personal data of EU individuals, adherence to the General Data Protection Regulation is non-negotiable. It ensures privacy and data rights are always respected.

These compliance frameworks create the necessary guardrails. As AI systems learn from your company’s processes and integrate with core systems, you know they are operating within a secure, auditable environment. This builds internal confidence for wider adoption and satisfies external regulatory scrutiny. To truly understand this balance, it helps to explore established frameworks for risk management and compliance for enterprise AI systems.

A Practical Roadmap for AI Deployment

Getting AI up and running isn’t a one-and-done event; it's a phased journey. You start small by identifying specific, high-impact workflows where automation can deliver obvious value, such as First Notice of Loss (FNOL) or simple AI customer care inquiries.

From that starting point, the process typically unfolds in a few key steps:

Process Mining and Training: The AI learns directly from your existing Standard Operating Procedures (SOPs) and historical data. It essentially observes how your best teams handle different scenarios, ensuring the AI’s logic aligns with your proven business practices.

System Integration: The AI platform connects to your existing core systems (like Guidewire or Duck Creek) and communication channels (like Genesys or Salesforce) through APIs. This creates a cohesive operational layer without forcing a painful rip-and-replace of your legacy tech.

Pilot and Refinement: The AI is deployed in a controlled pilot program. Performance is monitored closely, and feedback is gathered from the teams using it. Based on claims AI reviews and hard data, the models are fine-tuned for better accuracy and efficiency.

Scaling with Confidence: Once the pilot is a clear success and delivers a measurable ROI, the automation can be scaled to other teams and processes. This methodical approach minimizes disruption and ensures the technology is adopted safely and effectively.

By following a practical roadmap like this, insurers can bring in the power of AI to reinvent their operations while upholding the highest standards of safety and governance. It’s about building a resilient foundation for the future of insurance risk management.

9. Measuring the Success of Your AI Initiatives

So, you've invested in AI to automate claims and supercharge customer service. That's a big step. But how do you actually know if it’s paying off? To justify the investment and steer your strategy, you need to show leadership a clear, compelling return. This means going beyond simple cost savings and looking at a balanced set of metrics that tell the whole story.

Getting your measurement right allows AI insurance companies to prove gains in operational efficiency, customer experience, and, just as importantly, insurance risk management. By tracking the right Key Performance Indicators (KPIs), you can build a rock-solid business case, fine-tune your automated workflows, and show real value to everyone involved.

Key Metrics for Operational Efficiency

The first place you'll see the impact of AI automation is in your daily operations. These numbers are often the easiest to track and can provide quick wins to demonstrate ROI, especially when analyzing claims AI reviews.

Here are the heavy hitters for efficiency:

Claims Cycle Time: How long does it take to get from the First Notice of Loss (FNOL) to a settled claim? AI can take this from a multi-week headache to a matter of days—or even hours—for straightforward claims.

Loss Adjustment Expense (LAE): This is what it costs you to investigate and settle a claim. Automation drastically cuts down on the manual legwork for adjusters, which directly lowers this expense.

First Contact Resolution (FCR) Rate: When you deploy AI customer care, this metric shows how often the AI can solve a customer's issue without needing to pass it to a human. A high FCR is a win-win: lower costs for you, faster answers for them.

Quantifying the Customer Experience

A faster claims process is great, but only if it actually makes customers happier. Satisfied policyholders are the ones who stick around and tell their friends about you, making these metrics crucial for long-term health.

A seamless claims experience is the single most important moment for building customer loyalty. Measuring satisfaction here provides a direct look at the health of your customer relationships and the effectiveness of your AI-powered service delivery.

These customer-focused KPIs tell you if you're hitting the mark:

Net Promoter Score (NPS): This is the gold standard for measuring customer loyalty. It’s smart to specifically track the NPS of customers who have gone through an automated process. Their feedback tells you exactly how the tech is being received.

Customer Satisfaction (CSAT) Score: This gives you instant feedback on a specific interaction. A high CSAT score right after a policyholder gets an AI-powered claims update is a powerful sign that things are working.

Strengthening Risk Management Outcomes

Beyond just being faster and friendlier, AI brings serious muscle to your risk and compliance efforts. These metrics show how automation is fortifying your core processes, which is a fundamental goal of modern insurance risk management. For a deeper look at this, our article on data analytics in insurance explains how data is truly reshaping the industry.

Key KPIs for risk and compliance include:

Fraud Detection Rate: What percentage of fraudulent claims is the AI catching before a payout is made? Every tick upwards in this number is money saved.

Audit Trail Completeness: AI systems are meticulous record-keepers, creating a perfect, timestamped log of every single action. This KPI should be at 100%, giving you a completely auditable trail for regulators.

Compliance Adherence: This tracks how well the automated workflows stick to your predefined business rules and regulatory requirements, slashing the risk of expensive human errors.

Key Performance Indicators for AI in Insurance

To tie it all together, think of your metrics as a dashboard. It's not about one magic number; it's about seeing the complete picture. The table below summarizes the most critical KPIs you should be tracking to measure the true impact of AI across the business.

Category | Key Performance Indicator (KPI) | Description | Business Impact |

|---|---|---|---|

Operational Efficiency | Claims Cycle Time | Average time from FNOL to claim settlement. | Reduces operational costs, improves customer satisfaction. |

Operational Efficiency | Loss Adjustment Expense (LAE) | Cost to investigate and settle a claim. | Directly lowers claim processing costs, improving profitability. |

Operational Efficiency | First Contact Resolution (FCR) | Percentage of inquiries resolved by AI on the first try. | Lowers call center volume and operational overhead. |

Customer Experience | Net Promoter Score (NPS) | Measures customer loyalty and willingness to recommend. | Indicates long-term growth and brand health. |

Customer Experience | Customer Satisfaction (CSAT) | Measures satisfaction with a specific interaction. | Provides immediate feedback to improve service quality. |

Risk & Compliance | Fraud Detection Rate | Percentage of fraudulent claims identified before payment. | Prevents financial loss and protects the bottom line. |

Risk & Compliance | Audit Trail Completeness | Measures if every action is logged for regulatory review. | Ensures 100% compliance and reduces audit-related risks. |

Risk & Compliance | Compliance Adherence | Tracks adherence to internal and external regulations. | Minimizes risk of fines and legal penalties from human error. |

By tracking this balanced set of KPIs, you can move from "we think it's working" to "we can prove its value." This data-driven approach not only justifies the technology but also provides the critical insights needed to continuously improve and expand your automation strategy across the entire organization.

Common Questions About AI in Insurance Risk Management

As insurance leaders start seriously looking at AI, the same practical questions tend to pop up. It's only natural. People want to know about fairness, how it affects their teams, what the real financial return looks like, and how this new tech actually plugs into the systems they already have. Let's tackle these common questions head-on to give you a clear picture of how to approach AI in your insurance risk management strategy.

How Can We Ensure AI Decision-Making in Claims Is Fair and Unbiased?

This is arguably the most important question, and the answer starts long before the AI ever sees a live claim. You have to begin with the data itself. The historical data used to train any model needs a thorough audit to scrub it for hidden biases that could lead to unfair outcomes. If you don't, you're just teaching the machine to repeat past mistakes, only faster.

From there, the technology has to be transparent. That means building in what we call explainability (XAI) features, so you can always see why an AI recommended a certain action. Good governance is the final piece of the puzzle, especially a "human-in-the-loop" workflow for any significant decision.

For example, a platform like Nolana is designed with these operational guardrails from the ground up. An AI agent can handle the initial data gathering and fraud checks on a claim in seconds. But when it comes to a complex, high-value, or sensitive case, the final settlement decision is automatically routed to an experienced human adjuster. This blend of clean data, transparent tech, and human oversight is the bedrock of an ethical framework for AI insurance companies.

Will AI Replace Our Claims Adjusters and Customer Service Agents?

The goal isn't replacement; it's about making your best people even better. Think of AI as a force multiplier. It excels at the high-volume, repetitive, data-heavy tasks that often bog down your most talented professionals, freeing them up to focus on the work that truly requires a human touch—empathy, complex negotiation, and critical judgment. This shift is a cornerstone of modern insurance risk management.

Take an AI customer care scenario. An AI agent can instantly field thousands of basic policy questions, confirm coverage, or process a simple change of address. This frees up your human agents to dedicate their full attention to a policyholder who has just been in a major accident and needs genuine guidance and reassurance.

It's the same in claims. An AI can ingest photos from a car accident, analyze the damage, and flag potential fraud indicators in the time it takes to make a cup of coffee. This gives the human adjuster a complete, pre-vetted file from the get-go. They spend less time chasing paperwork and more time on the high-stakes parts of their job. In this model, AI isn't a replacement; it's a powerful co-pilot.

What Is the Typical ROI for AI Claims and Customer Care Automation?

When you automate claims and customer care, the return on investment (ROI) shows up in a few key areas. You'll often see these metrics pop up in claims AI reviews because they're the clearest signs of a successful program.

The financial upside breaks down into three main buckets:

Operational Cost Reduction: Automating manual work like data entry, document checks, and routine customer queries can cut operational costs in those specific workflows by 30-50%.

Efficiency and Speed: AI just moves faster. Claims that used to drag on for weeks can often be wrapped up in days or even hours. This not only makes customers happier but also drives down the loss adjustment expenses (LAE) associated with each claim.

Improved Risk Outcomes: Today’s AI algorithms are simply better and faster at spotting fraud than manual reviews alone. Catching even a small percentage of fraudulent payouts can save an organization millions, protecting the bottom line directly.

Most leading AI insurance companies find they achieve a tangible, positive ROI within 12 to 24 months as they roll out automation across more of their business.

How Do We Integrate an AI Platform with Our Existing Core Systems?

The fear of a massive, disruptive "rip and replace" project is one of the biggest things holding IT leaders back. Thankfully, modern AI platforms are built specifically to avoid that nightmare. They're designed for smooth integration with the core insurance systems you already rely on, like Guidewire or Duck Creek.

The magic here is in the APIs (Application Programming Interfaces) and libraries of pre-built connectors. An agentic AI platform like Nolana acts as an intelligent layer that sits on top of your existing tech stack. It can pull data from one system, use its logic to make a decision, and then push an action into another system—all without you having to re-architect anything.

This API-first approach means you can start automating processes and see value almost immediately, without bringing core operations to a halt. The AI platform works with the systems you have, making implementation faster, less risky, and far more agile.

This lets you modernize your operations and sharpen your insurance risk management capabilities without the pain and expense of replacing the legacy systems your business was built on.

Ready to transform your insurance operations with compliant, efficient AI automation? Nolana deploys intelligent AI agents trained on your processes to automate claims, customer care, and more, all while keeping your team in full control. Discover how Nolana can help you reduce costs and improve customer satisfaction.

For a long time, insurance risk management was seen as a purely defensive game—a necessary cost center focused on preventing losses. That view is officially outdated. Today, for any insurer looking to grow, it's about turning risk into a strategic advantage, helping navigate economic turbulence and meet sky-high customer expectations.

The New Era of Insurance Risk Management

The modern insurance world is a pressure cooker. We're facing everything from escalating catastrophe losses to a hyper-competitive market that leaves zero room for error. In this environment, the most forward-thinking AI insurance companies aren't just using technology for a bit of efficiency. They're weaving it into the very fabric of their risk strategy.

Think of it like a captain navigating a complex shipping route. A basic radar helps you avoid icebergs (the old way of seeing risk). But an advanced, AI-powered navigation system? That not only steers you clear of danger but also charts the fastest, most fuel-efficient path to your destination, revealing opportunities you never knew existed.

This proactive mindset is no longer optional; it's essential for survival. The industry is staring down a massive and growing "protection gap," where the economic fallout from disasters wildly outstrips what's actually insured. This puts immense strain on the old ways of doing business.

Navigating Unprecedented Volatility

The numbers really tell the story here. In a recent year, natural catastrophes caused an estimated $357 billion in economic losses. The shocking part? Only about 35% of that was insured.

That left a staggering $234 billion protection gap, a clear signal that the industry's existing capacity and models are being stretched to their limits. And the volatility is only getting worse. In the first half of the following year, insured losses from natural disasters shot past $100 billion, a jarring 40% jump from the year before. This isn't a minor fluctuation; it's a trend that demands a complete rethink of how we handle risk, capital, and pricing.

Regulators are taking notice. They're now flagging climate-related exposures, persistent cyber threats, and geopolitical instability as top-tier concerns, pushing insurers to get much more sophisticated with their scenario analysis and cross-border planning.

AI as the New Bedrock of Operations

So, how do you manage these pressures without buckling? The answer lies in smarter operations, powered by automation. AI is quickly becoming the go-to solution for overhauling two of the most critical functions in financial services: claims processing and customer care.

By automating the intricate, often frustrating workflows in these areas, insurers can slash cycle times, boost accuracy, and build the kind of customer loyalty that was once impossible to achieve at scale. This isn't just about managing day-to-day tasks; it's a fundamental part of building a more resilient and profitable business. You can learn more about how risk management is applied in operations in our detailed guide.

Platforms that deliver on AI customer care and claims automation are no longer a "nice-to-have." They are the foundation for the future of insurance.

Building a Resilient ERM Framework

Think of a modern Enterprise Risk Management (ERM) framework as the essential blueprint for any successful insurer. It’s what transforms risk management from a scattered, reactive scramble into a unified, firm-wide strategy. This framework is the structure that gives you the discipline and foresight needed to navigate the complexities of underwriting, pricing, and claims.

At the heart of any strong ERM is a clearly defined risk appetite. This isn't just a number; it’s a guiding philosophy. It clearly states the amount and type of risk your organization is willing to take on to hit its strategic goals. Without it, an insurer is essentially flying blind, unable to tell the difference between a calculated risk and a reckless gamble.

Navigating Market Cycles and Pricing Pressures

This disciplined approach is absolutely critical when market conditions shift—and they always do. Take the commercial insurance pricing cycle, for instance. It can force dramatic changes in underwriting tactics. We saw this recently when the market softened considerably, with one report noting a 4% drop in global commercial insurance rates in a single quarter, ending a seven-year streak of increases.

That kind of shift signals intense competition and a flood of capacity, which puts direct pressure on premiums and underwriting margins. In response, many insurers are pulling back on their risk-taking. A recent survey found that only 12% of insurers were looking to increase risk, while 67% were actively exploring alternative capital structures like reinsurance sidecars to better manage their exposures. These are the kinds of measurable market movements that force carriers to get much sharper with their risk selection and expand their capital management toolkit just to stay profitable.

The chart below shows how a modern risk framework can integrate technology, like AI, to build resilience and drive growth, even in a tough market.

This visual really clarifies the hierarchy: foundational risk management principles are amplified by AI and technology, which together enable a company to grow and become more resilient.

The Three Lines of Defense Model

To actually put a framework like this into practice, leading insurers rely on the "three lines of defense" model. It’s a governance structure that clarifies exactly who is responsible for what when it comes to managing risk across the entire organization.

First Line: This is your front line—the business operations teams like underwriters and claims handlers. They own and manage their risks directly and are responsible for identifying and controlling them day-to-day.

Second Line: The risk management and compliance functions act as the second line. They provide oversight, setting the policies and frameworks that guide the first line's activities.

Third Line: Internal audit serves as the independent third line. They provide objective assurance that the first two lines are working effectively and that the overall framework is sound.

This model is all about accountability. It creates a system of checks and balances that prevents critical risks from falling through the cracks, which is vital for maintaining stability, especially as more core processes become automated.

By using a well-defined framework to assess potential threats, you can establish clear priorities for mitigation. For a practical look at how this works, you can see a risk assessment form template AI-generated example to better understand the process.

How AI Is Transforming Claims And Customer Care

For decades, the insurance claims process has been a major friction point. It's often slow, manual, and frankly, a frustrating experience for everyone involved—policyholders and insurers alike. Artificial intelligence is now completely flipping that script. We're moving away from reactive, paper-heavy workflows and toward automated, proactive systems that are a game-changer for insurance risk management.

This isn't just about shaving off a few operational costs. By automating core tasks, AI is fundamentally redefining what's possible in speed, accuracy, and customer satisfaction. The entire journey of a claim, from the first call to the final payment, is being rebuilt from the ground up for a smarter, more efficient world.

This is the new front line of claims. A customer can now snap a photo, and that simple action can trigger a fully automated assessment, feeding data straight into an intelligent workflow.

Automating The Claims Lifecycle With AI

The claims experience is the moment of truth for any insurer. A clunky, drawn-out process can shatter a customer relationship in an instant. But a fast, transparent, and simple one can build loyalty that lasts a lifetime. AI agents are now being deployed at every single stage of this critical journey.

Here’s where the automation is making the biggest impact:

First Notice of Loss (FNOL): AI chatbots and voice assistants work around the clock, handling the initial claim intake 24/7. They gather all the essential details and documents, so a human adjuster doesn't have to.

Damage Assessment: Forget waiting for an adjuster to schedule a visit. Computer vision AI can analyze photos and videos of damage to a car or home, generating a repair estimate almost instantly.

Fraud Detection: AI algorithms are incredibly good at spotting red flags. They can sift through thousands of data points in real-time to identify suspicious patterns that a person would almost certainly miss.

Settlement and Payment: For straightforward claims, AI can run the show from start to finish, automating settlement and getting money into a policyholder's hands in a matter of hours, not weeks.

This rapid shift toward AI is also forcing a rethink of operational risk. One recent survey found that 55% of insurers now list risk management and analytics as a top investment priority. Insurers are pouring money into better data and automation to shrink loss ratios, but they're also wisely investing in the governance and control systems needed to ensure AI doesn't introduce brand-new risks.

Delivering Superior AI Customer Care

The impact of AI extends well beyond just claims. It’s also completely changing the game for customer service in financial services. Today’s policyholders expect immediate, helpful answers, and AI is delivering.

Instead of sitting on hold, customers can now interact with intelligent AI agents that provide instant, personalized support. These agents can tap into an insurer’s entire knowledge base to answer complex policy questions, process account changes, or even offer advice on coverage—all with a consistent and helpful tone.

A smart "human-in-the-loop" design is key here. The AI handles the high volume of routine questions, but it’s trained to know exactly when to escalate a conversation to a human expert for situations that require real empathy or complex judgment.

This frees up human agents to focus on the high-stakes, emotionally charged interactions where their expertise truly matters. The payoff is a much better customer experience, which shows up in higher Net Promoter Scores (NPS). To see how this works in practice, you can get more details in our guide on AI in insurance claims.

The table below shows a clear before-and-after picture of how AI-powered platforms like Nolana are overhauling traditional insurance operations.

AI Impact on Insurance Operations

Operational Area | Traditional Process (Manual) | AI-Automated Process (e.g., with Nolana) | Key Performance Indicator (KPI) Impact |

|---|---|---|---|

Claims Intake (FNOL) | Phone calls, manual data entry, business hours only. | 24/7 intake via chatbot/voice, automated data extraction. | -30% call center volume, +50% intake speed. |

Damage Assessment | Manual review by adjusters, scheduling physical inspections. | Instant analysis of photos/videos with computer vision AI. | -90% assessment time (days to minutes). |

Fraud Detection | Manual review, reliance on adjuster suspicion. | Real-time analysis of claim data to flag anomalies. | +25% fraud detection rate, reduced false positives. |

Customer Service | Long hold times, agent-dependent knowledge, limited hours. | Instant 24/7 support, AI-powered knowledge base access. | -40% in operational costs, +20% NPS. |

As you can see, the improvements aren't just incremental; they represent a fundamental shift in efficiency, accuracy, and customer satisfaction across the board.

The Power Of Integration And Fraud Prevention

Of course, for any of this to work, AI systems have to play nice with an insurer's existing core platforms, like Guidewire or Duck Creek. This is where modern agentic platforms like Nolana shine. They are designed to act as an intelligent layer that sits on top of legacy technology. This means they can pull information, help with decisions, and execute tasks without forcing a hugely expensive and disruptive "rip-and-replace" project.

This integration also bolsters one of AI’s most powerful applications: fraud prevention. By connecting disparate systems, AI can verify identities and authenticate documents with incredible precision. For example, new tools are using a Bluenotary's biometric-first approach to reducing fraud risk to add a serious layer of security to digital claims. By automating these crucial checks, insurers can manage risk far more effectively, protecting their bottom line and their honest customers.

Implementing AI Safely in a Regulated Industry

Bringing artificial intelligence into a field as heavily regulated as insurance is about much more than just plugging in new software. You’re navigating a careful balance between earning trust, proving the tech is reliable, and making sure every single automated action meets strict compliance standards. For AI insurance companies, the only path forward is one built on strong governance and a clear, responsible strategy.

What this really means is building a framework where AI doesn’t just operate inside a black box. Every decision must be traceable, explainable, and fully auditable. This is where concepts like Explainable AI (XAI) become so critical, giving risk and compliance teams the ability to see the "why" behind any AI-driven recommendation.

Building a Human-in-the-Loop System

There's a common myth that AI automation is all about replacing people. In a high-stakes industry like insurance, nothing could be further from the truth. The most effective—and safest—approach is a "human-in-the-loop" system, where AI and human experts work together, each playing to their own unique strengths.

Think of it as a finely tuned partnership. AI agents can chew through high-volume, data-heavy tasks with incredible speed and accuracy, like reviewing initial claim documents, flagging potential fraud indicators, or handling routine policy questions. But they operate with very clear guardrails.

The moment a case involves unusual complexity, high financial stakes, or requires a dose of genuine human empathy, the AI is programmed to seamlessly escalate it to a person. This ensures that while routine work gets automated, critical judgment always stays in human hands—a cornerstone of responsible insurance risk management.

This blended approach isn’t just a safety net; it’s a powerful strategic advantage. It frees up your skilled adjusters and service agents to focus their expertise on the most complex and valuable work, which ultimately improves both efficiency and customer outcomes.

The Critical Role of Governance and Compliance

For any insurer, deploying AI without an ironclad compliance foundation is simply not an option. Regulators demand transparency, and customers (rightfully) expect their data to be handled with the utmost security. This is precisely why platforms designed for regulated industries are built with compliance baked in from the very start.

Agentic platforms like Nolana, for example, are architected to meet rigorous standards from day one. This means achieving certifications that are table stakes for earning enterprise trust.

SOC 2 Compliance: This is proof of a commitment to securely managing customer data to protect both your organization and your clients' privacy. You can get a better sense of its importance by learning about what SOC 2 compliance is and why it’s a benchmark for any serious service provider.

GDPR Compliance: For any insurer touching the personal data of EU individuals, adherence to the General Data Protection Regulation is non-negotiable. It ensures privacy and data rights are always respected.

These compliance frameworks create the necessary guardrails. As AI systems learn from your company’s processes and integrate with core systems, you know they are operating within a secure, auditable environment. This builds internal confidence for wider adoption and satisfies external regulatory scrutiny. To truly understand this balance, it helps to explore established frameworks for risk management and compliance for enterprise AI systems.

A Practical Roadmap for AI Deployment

Getting AI up and running isn’t a one-and-done event; it's a phased journey. You start small by identifying specific, high-impact workflows where automation can deliver obvious value, such as First Notice of Loss (FNOL) or simple AI customer care inquiries.

From that starting point, the process typically unfolds in a few key steps:

Process Mining and Training: The AI learns directly from your existing Standard Operating Procedures (SOPs) and historical data. It essentially observes how your best teams handle different scenarios, ensuring the AI’s logic aligns with your proven business practices.

System Integration: The AI platform connects to your existing core systems (like Guidewire or Duck Creek) and communication channels (like Genesys or Salesforce) through APIs. This creates a cohesive operational layer without forcing a painful rip-and-replace of your legacy tech.

Pilot and Refinement: The AI is deployed in a controlled pilot program. Performance is monitored closely, and feedback is gathered from the teams using it. Based on claims AI reviews and hard data, the models are fine-tuned for better accuracy and efficiency.

Scaling with Confidence: Once the pilot is a clear success and delivers a measurable ROI, the automation can be scaled to other teams and processes. This methodical approach minimizes disruption and ensures the technology is adopted safely and effectively.

By following a practical roadmap like this, insurers can bring in the power of AI to reinvent their operations while upholding the highest standards of safety and governance. It’s about building a resilient foundation for the future of insurance risk management.

9. Measuring the Success of Your AI Initiatives

So, you've invested in AI to automate claims and supercharge customer service. That's a big step. But how do you actually know if it’s paying off? To justify the investment and steer your strategy, you need to show leadership a clear, compelling return. This means going beyond simple cost savings and looking at a balanced set of metrics that tell the whole story.

Getting your measurement right allows AI insurance companies to prove gains in operational efficiency, customer experience, and, just as importantly, insurance risk management. By tracking the right Key Performance Indicators (KPIs), you can build a rock-solid business case, fine-tune your automated workflows, and show real value to everyone involved.

Key Metrics for Operational Efficiency

The first place you'll see the impact of AI automation is in your daily operations. These numbers are often the easiest to track and can provide quick wins to demonstrate ROI, especially when analyzing claims AI reviews.

Here are the heavy hitters for efficiency:

Claims Cycle Time: How long does it take to get from the First Notice of Loss (FNOL) to a settled claim? AI can take this from a multi-week headache to a matter of days—or even hours—for straightforward claims.

Loss Adjustment Expense (LAE): This is what it costs you to investigate and settle a claim. Automation drastically cuts down on the manual legwork for adjusters, which directly lowers this expense.

First Contact Resolution (FCR) Rate: When you deploy AI customer care, this metric shows how often the AI can solve a customer's issue without needing to pass it to a human. A high FCR is a win-win: lower costs for you, faster answers for them.

Quantifying the Customer Experience

A faster claims process is great, but only if it actually makes customers happier. Satisfied policyholders are the ones who stick around and tell their friends about you, making these metrics crucial for long-term health.

A seamless claims experience is the single most important moment for building customer loyalty. Measuring satisfaction here provides a direct look at the health of your customer relationships and the effectiveness of your AI-powered service delivery.

These customer-focused KPIs tell you if you're hitting the mark:

Net Promoter Score (NPS): This is the gold standard for measuring customer loyalty. It’s smart to specifically track the NPS of customers who have gone through an automated process. Their feedback tells you exactly how the tech is being received.

Customer Satisfaction (CSAT) Score: This gives you instant feedback on a specific interaction. A high CSAT score right after a policyholder gets an AI-powered claims update is a powerful sign that things are working.

Strengthening Risk Management Outcomes

Beyond just being faster and friendlier, AI brings serious muscle to your risk and compliance efforts. These metrics show how automation is fortifying your core processes, which is a fundamental goal of modern insurance risk management. For a deeper look at this, our article on data analytics in insurance explains how data is truly reshaping the industry.

Key KPIs for risk and compliance include:

Fraud Detection Rate: What percentage of fraudulent claims is the AI catching before a payout is made? Every tick upwards in this number is money saved.

Audit Trail Completeness: AI systems are meticulous record-keepers, creating a perfect, timestamped log of every single action. This KPI should be at 100%, giving you a completely auditable trail for regulators.

Compliance Adherence: This tracks how well the automated workflows stick to your predefined business rules and regulatory requirements, slashing the risk of expensive human errors.

Key Performance Indicators for AI in Insurance

To tie it all together, think of your metrics as a dashboard. It's not about one magic number; it's about seeing the complete picture. The table below summarizes the most critical KPIs you should be tracking to measure the true impact of AI across the business.

Category | Key Performance Indicator (KPI) | Description | Business Impact |

|---|---|---|---|

Operational Efficiency | Claims Cycle Time | Average time from FNOL to claim settlement. | Reduces operational costs, improves customer satisfaction. |

Operational Efficiency | Loss Adjustment Expense (LAE) | Cost to investigate and settle a claim. | Directly lowers claim processing costs, improving profitability. |

Operational Efficiency | First Contact Resolution (FCR) | Percentage of inquiries resolved by AI on the first try. | Lowers call center volume and operational overhead. |

Customer Experience | Net Promoter Score (NPS) | Measures customer loyalty and willingness to recommend. | Indicates long-term growth and brand health. |

Customer Experience | Customer Satisfaction (CSAT) | Measures satisfaction with a specific interaction. | Provides immediate feedback to improve service quality. |

Risk & Compliance | Fraud Detection Rate | Percentage of fraudulent claims identified before payment. | Prevents financial loss and protects the bottom line. |

Risk & Compliance | Audit Trail Completeness | Measures if every action is logged for regulatory review. | Ensures 100% compliance and reduces audit-related risks. |

Risk & Compliance | Compliance Adherence | Tracks adherence to internal and external regulations. | Minimizes risk of fines and legal penalties from human error. |

By tracking this balanced set of KPIs, you can move from "we think it's working" to "we can prove its value." This data-driven approach not only justifies the technology but also provides the critical insights needed to continuously improve and expand your automation strategy across the entire organization.

Common Questions About AI in Insurance Risk Management

As insurance leaders start seriously looking at AI, the same practical questions tend to pop up. It's only natural. People want to know about fairness, how it affects their teams, what the real financial return looks like, and how this new tech actually plugs into the systems they already have. Let's tackle these common questions head-on to give you a clear picture of how to approach AI in your insurance risk management strategy.

How Can We Ensure AI Decision-Making in Claims Is Fair and Unbiased?

This is arguably the most important question, and the answer starts long before the AI ever sees a live claim. You have to begin with the data itself. The historical data used to train any model needs a thorough audit to scrub it for hidden biases that could lead to unfair outcomes. If you don't, you're just teaching the machine to repeat past mistakes, only faster.

From there, the technology has to be transparent. That means building in what we call explainability (XAI) features, so you can always see why an AI recommended a certain action. Good governance is the final piece of the puzzle, especially a "human-in-the-loop" workflow for any significant decision.

For example, a platform like Nolana is designed with these operational guardrails from the ground up. An AI agent can handle the initial data gathering and fraud checks on a claim in seconds. But when it comes to a complex, high-value, or sensitive case, the final settlement decision is automatically routed to an experienced human adjuster. This blend of clean data, transparent tech, and human oversight is the bedrock of an ethical framework for AI insurance companies.

Will AI Replace Our Claims Adjusters and Customer Service Agents?

The goal isn't replacement; it's about making your best people even better. Think of AI as a force multiplier. It excels at the high-volume, repetitive, data-heavy tasks that often bog down your most talented professionals, freeing them up to focus on the work that truly requires a human touch—empathy, complex negotiation, and critical judgment. This shift is a cornerstone of modern insurance risk management.

Take an AI customer care scenario. An AI agent can instantly field thousands of basic policy questions, confirm coverage, or process a simple change of address. This frees up your human agents to dedicate their full attention to a policyholder who has just been in a major accident and needs genuine guidance and reassurance.

It's the same in claims. An AI can ingest photos from a car accident, analyze the damage, and flag potential fraud indicators in the time it takes to make a cup of coffee. This gives the human adjuster a complete, pre-vetted file from the get-go. They spend less time chasing paperwork and more time on the high-stakes parts of their job. In this model, AI isn't a replacement; it's a powerful co-pilot.

What Is the Typical ROI for AI Claims and Customer Care Automation?

When you automate claims and customer care, the return on investment (ROI) shows up in a few key areas. You'll often see these metrics pop up in claims AI reviews because they're the clearest signs of a successful program.

The financial upside breaks down into three main buckets:

Operational Cost Reduction: Automating manual work like data entry, document checks, and routine customer queries can cut operational costs in those specific workflows by 30-50%.

Efficiency and Speed: AI just moves faster. Claims that used to drag on for weeks can often be wrapped up in days or even hours. This not only makes customers happier but also drives down the loss adjustment expenses (LAE) associated with each claim.

Improved Risk Outcomes: Today’s AI algorithms are simply better and faster at spotting fraud than manual reviews alone. Catching even a small percentage of fraudulent payouts can save an organization millions, protecting the bottom line directly.

Most leading AI insurance companies find they achieve a tangible, positive ROI within 12 to 24 months as they roll out automation across more of their business.

How Do We Integrate an AI Platform with Our Existing Core Systems?

The fear of a massive, disruptive "rip and replace" project is one of the biggest things holding IT leaders back. Thankfully, modern AI platforms are built specifically to avoid that nightmare. They're designed for smooth integration with the core insurance systems you already rely on, like Guidewire or Duck Creek.

The magic here is in the APIs (Application Programming Interfaces) and libraries of pre-built connectors. An agentic AI platform like Nolana acts as an intelligent layer that sits on top of your existing tech stack. It can pull data from one system, use its logic to make a decision, and then push an action into another system—all without you having to re-architect anything.

This API-first approach means you can start automating processes and see value almost immediately, without bringing core operations to a halt. The AI platform works with the systems you have, making implementation faster, less risky, and far more agile.

This lets you modernize your operations and sharpen your insurance risk management capabilities without the pain and expense of replacing the legacy systems your business was built on.

Ready to transform your insurance operations with compliant, efficient AI automation? Nolana deploys intelligent AI agents trained on your processes to automate claims, customer care, and more, all while keeping your team in full control. Discover how Nolana can help you reduce costs and improve customer satisfaction.

Want early access?

© 2026 Nolana Limited. All rights reserved.

Leroy House, Unit G01, 436 Essex Rd, London N1 3QP

Want early access?

© 2026 Nolana Limited. All rights reserved.

Leroy House, Unit G01, 436 Essex Rd, London N1 3QP

Want early access?

© 2026 Nolana Limited. All rights reserved.

Leroy House, Unit G01, 436 Essex Rd, London N1 3QP

Want early access?

© 2026 Nolana Limited. All rights reserved.

Leroy House, Unit G01, 436 Essex Rd, London N1 3QP